Sys.setenv(OMP_THREAD_LIMIT = 1) # Reducing core use, to avoid accidental use of too many cores

library(Colossus)

library(data.table)

#>

#> Attaching package: 'data.table'

#> The following object is masked from 'package:base':

#>

#> %notin%

if (system.file(package = "survival") != "") {

library(survival)

}

library(dplyr)

#>

#> Attaching package: 'dplyr'

#> The following objects are masked from 'package:data.table':

#>

#> between, first, last

#> The following objects are masked from 'package:stats':

#>

#> filter, lag

#> The following objects are masked from 'package:base':

#>

#> intersect, setdiff, setequal, unionAvailable Methods

Colossus supports two methods of calculating a

confidence interval for model parameters for Cox proportional hazards

models. The Wald method and a likelihood-based boundary method. This

vignette will be focused on the differences and what issues may

arise.

Wald Method

When Colossus finishes a Cox regression, it returns both

parameter estimates and standard errors. The simplest form of confidence

interval is assuming a normal distribution with the parameter mean and

deviation. The standard errors are calculated from the covariance

matrix, which is calculated in line with the equation for the expected

information matrix presented in the 32-bit Epicure manual. The

covariance matrix is calculated using the inverse of the expected

information matrix

().

The derivation is outlined at the end of this vignette for clarity.

For every event time

()

there are a number of events

()

and a list of subjects at risk

().

Every valid combination of subject and event time has a hazard ratio

()

and a partial derivative of the hazard ratio with respect to each

parameter

().

This equation is used to compute the covariance matrix and standard

errors returned by Colossus by default.

This gives a symmetric parameter confidence interval which is often accurate for single-term log-linear models. However, this approximation is often inaccurate for models with linear effects, particularly if the confidence interval includes negative values. Because the Wald method approximates the likelihood confidence interval, there is no guarantee that the model is defined over the interval.

Likelihood-Based Bound

The more exact solution is to directly solve for the boundary. The

basic premise is that the model can be optimized with a single parameter

()

fixed. Each value of

has a corresponding maximum log-likelihood. The confidence interval is

the range of values of

such that the maximum log-likelihood is above a threshold, taken from

the asymptotic

distribution of the generalized likelihood ratio test.

Colossus uses the Venzon-Moolgavkar algorithm to

iteratively solve for the interval endpoints.

There is one main issue that can arise from this method: this uses a

Newton-Raphson algorithm, which may solve for local solutions instead of

the global solution. Similar to the general Colossus

regressions, limitations can be placed on step size to limit these

effects. However, there is no analog to selecting multiple starting

locations. This is the basis for alternatives provided that can more

directly solve for the true optimum. Methods have been implemented to

optimize multiple points and apply a bisection method instead of a

derivative-based method.

This method directly solves the confidence interval, which for linear cases may be non-symmetric or even not have upper or lower bounds. Linear models may be defined only above a parameter threshold. If the optimum value at that parameter threshold is above the threshold value, then the interval would not have a lower bound.

Example and Comparison

For the sake of comparison, we will consider an analysis of the

capacitor data available in the survival package. Consider

the two regressions, one fully exponential and one with a linear effect.

Both regressions converge with similar scores.

if (system.file(package = "survival") != "") {

data(reliability, package = "survival")

capacitor |> setDT()

df <- copy(capacitor)

} else {

voltage <- c(200, 200, 200, 200, 250, 250, 250, 250, 300, 300, 300, 300, 350, 350, 350, 350, 200, 200, 200, 200, 250, 250, 250, 250, 300, 300, 300, 300, 350, 350, 350, 350, 200, 200, 200, 200, 250, 250, 250, 250, 300, 300, 300, 300, 350, 350, 350, 350, 200, 200, 200, 200, 250, 250, 250, 250, 300, 300, 300, 300, 350, 350, 350, 350)

temperature <- c(170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 170, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180, 180)

time <- c(439, 904, 1092, 1105, 572, 690, 904, 1090, 315, 315, 439, 628, 258, 258, 347, 588, 959, 1065, 1065, 1087, 216, 315, 455, 473, 241, 315, 332, 380, 241, 241, 435, 455, 1105, 1105, 1105, 1105, 1090, 1090, 1090, 1090, 628, 628, 628, 628, 588, 588, 588, 588, 1087, 1087, 1087, 1087, 473, 473, 473, 473, 380, 380, 380, 380, 455, 455, 455, 455)

status <- c(1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0)

df <- data.table(

voltage = voltage,

temperature = temperature,

time = time,

status = status

)

}

df$voltage <- (df$voltage - 200) / 150

df$temperature <- (df$temperature - 170) / 10

df$time <- (df$time - 216) / (1105 - 216)

control <- list(ncores = 1, maxiter = 100, verbose = 2)

a_n <- c(0.01, 0.01)

e1 <- CoxRun(Cox(time, status) ~ loglinear(temperature, voltage, 0), df,

a_n = a_n, control = control

)

print(e1, 5)

#> |--------------------------------------------------------------------------------|

#> Final Results

#> Covariate Subterm Central Estimate Standard Error 95% Confidence Interval

#> <char> <char> <num> <num> <char>

#> 1: temperature loglin 0.7597 0.39643 (-0.017298 - 1.5367)

#> 2: voltage loglin 1.9872 0.60622 (0.798951 - 3.1754)

#> 2-tail p-value

#> <num>

#> 1: 0.0553188

#> 2: 0.0010458

#> |- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -|

#>

#> Cox Model Used

#> Survival Age Column was: 'time', Outcome Column was: 'status'

#> Risk Groups Used: 22

#> |- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -|

#> -2*Log-Likelihood: 210.77793, AIC: 214.77793

#> Iterations run: 5

#> maximum step size: 3.76854e-03, maximum first derivative: 3.34296e-03

#> Last iteration improved the log-likelihood by: 3.28859e-05

#> Analysis converged

#> Records Used: 64, Records Removed: 0

#> Run finished in 0.03173 seconds

#> |--------------------------------------------------------------------------------|

e2 <- CoxRun(Cox(time, status) ~ loglinear(temperature, 0) + plinear(voltage, 0),

df,

a_n = a_n, control = control

)

print(e2, 5)

#> |--------------------------------------------------------------------------------|

#> Final Results

#> Covariate Subterm Central Estimate Standard Error 95% Confidence Interval

#> <char> <char> <num> <num> <char>

#> 1: temperature loglin 0.95011 0.43126 (0.10485 - 1.7954)

#> 2: voltage plin 8.80439 6.18152 (-3.31138 - 20.9202)

#> 2-tail p-value

#> <num>

#> 1: 0.027586

#> 2: 0.154357

#> |- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -|

#>

#> Cox Model Used

#> Survival Age Column was: 'time', Outcome Column was: 'status'

#> Risk Groups Used: 22

#> |- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -|

#> -2*Log-Likelihood: 208.49028, AIC: 212.49028

#> Iterations run: 11

#> maximum step size: 3.96072e-02, maximum first derivative: 5.76358e-04

#> Last iteration improved the log-likelihood by: 3.57097e-05

#> Analysis converged

#> Records Used: 64, Records Removed: 0

#> Run finished in 0.0192 seconds

#> |--------------------------------------------------------------------------------|Next, suppose we were interested in the confidence intervals. Suppose we want 95% confidence intervals for both the Wald and likelihood-based boundaries and for both parameters in each model.

Let us start with the fully exponential model. The Wald boundary is

estimated using the central estimates and standard deviations. The

Likelihood boundary is solved using the LikelihoodBound()

function applied to the result. The parameter number needs to be

provided (indexed starting at one) and an alpha level needs to be

provided.

Overall, the Wald and likelihood-based boundaries are not the same. The boundaries for temperature are (-0.017, 1.537) and (-0.01, 1.560), and the boundaries for voltage are (0.800, 3.177) and (0.841, 3.242). The two boundaries are off by less than 0.1.

names <- c("temperature", "voltage")

tform <- c("loglin", "loglin")

ci_1 <- c(

e1$beta_0[1] - 1.96 * e1$Standard_Error[1],

e1$beta_0[1] + 1.96 * e1$Standard_Error[1]

)

ci_2 <- c(

e1$beta_0[2] - 1.96 * e1$Standard_Error[2],

e1$beta_0[2] + 1.96 * e1$Standard_Error[2]

)

curve_control <- list(

maxstep = 100,

alpha = 0.05,

para_number = 1, manual = TRUE

)

e <- LikelihoodBound(e1, df, curve_control, control = control)

cat("|------------------- Wald Estimate -------------------|")

#> |------------------- Wald Estimate -------------------|

print(ci_1)

#> [1] -0.01729844 1.53669709

print(e, 5)

#> |--------------------------------------------------------------------------------|

#> Likelihood Boundary Results

#> Proportional Hazards Model

#> Solving for the boundary of element: 1

#> Applied to column: 'temperature'

#> Subterm: loglin

#> Term number: 0

#> Lower limit converged to at -0.0098972 at a score of -107.30968 with of goal of -107.30969

#> Central estimate was 0.7597

#> Upper limit converged to at 1.5599 at a score of -107.30968 with of goal of -107.30969

#> Run finished in 0.01266 seconds

#> |--------------------------------------------------------------------------------|

curve_control <- list(

maxstep = 100,

alpha = 0.05,

para_number = 2, manual = TRUE

)

e <- LikelihoodBound(e1, df, curve_control, control = control)

cat("|------------------- Likelihood Bound Estimate -------------------|")

#> |------------------- Likelihood Bound Estimate -------------------|

print(ci_2)

#> [1] 0.7989513 3.1753506

print(e, 5)

#> |--------------------------------------------------------------------------------|

#> Likelihood Boundary Results

#> Proportional Hazards Model

#> Solving for the boundary of element: 2

#> Applied to column: 'voltage'

#> Subterm: loglin

#> Term number: 0

#> Lower limit converged to at 0.84123 at a score of -107.30968 with of goal of -107.30969

#> Central estimate was 1.9872

#> Upper limit converged to at 3.242 at a score of -107.30968 with of goal of -107.30969

#> Run finished in 0.01212 seconds

#> |--------------------------------------------------------------------------------|Next, we analyze a model with a linear effect. We would expect the predictions to be further off. The boundaries for temperature are (0.105, 1.796) and (0.129, 1.840), and the boundaries for voltage are (-3.32, 20.95) and (1.97, 34.472). The estimates for the temperature and voltage boundaries are much further off.

ci_1 <- c(

e2$beta_0[1] - 1.96 * e2$Standard_Error[1],

e2$beta_0[1] + 1.96 * e2$Standard_Error[1]

)

ci_2 <- c(

e2$beta_0[2] - 1.96 * e2$Standard_Error[2],

e2$beta_0[2] + 1.96 * e2$Standard_Error[2]

)

curve_control <- list(

maxstep = 100,

alpha = 0.05,

para_number = 1, manual = TRUE

)

e <- LikelihoodBound(e2, df, curve_control, control = control)

cat("|------------------- Wald Estimate -------------------|")

#> |------------------- Wald Estimate -------------------|

print(ci_1)

#> [1] 0.1048487 1.7953696

print(e, 5)

#> |--------------------------------------------------------------------------------|

#> Likelihood Boundary Results

#> Proportional Hazards Model

#> Solving for the boundary of element: 1

#> Applied to column: 'temperature'

#> Subterm: loglin

#> Term number: 0

#> Lower limit converged to at 0.12897 at a score of -106.16586 with of goal of -106.16587

#> Central estimate was 0.95011

#> Upper limit converged to at 1.8401 at a score of -106.16587 with of goal of -106.16587

#> Run finished in 0.01286 seconds

#> |--------------------------------------------------------------------------------|

a_n <- c(1.138152, 1.988403)

curve_control <- list(

maxstep = 100,

alpha = 0.05,

para_number = 2, manual = TRUE

)

e <- LikelihoodBound(e2, df, curve_control, control = control)

cat("|------------------- Wald Estimate -------------------|")

#> |------------------- Wald Estimate -------------------|

print(ci_2)

#> [1] -3.311383 20.920163

print(e, 5)

#> |--------------------------------------------------------------------------------|

#> Likelihood Boundary Results

#> Proportional Hazards Model

#> Solving for the boundary of element: 2

#> Applied to column: 'voltage'

#> Subterm: plin

#> Term number: 0

#> Lower limit converged to at 1.9709 at a score of -106.16585 with of goal of -106.16587

#> Central estimate was 8.8044

#> Upper limit converged to at 34.471 at a score of -106.16586 with of goal of -106.16587

#> Run finished in 0.01348 seconds

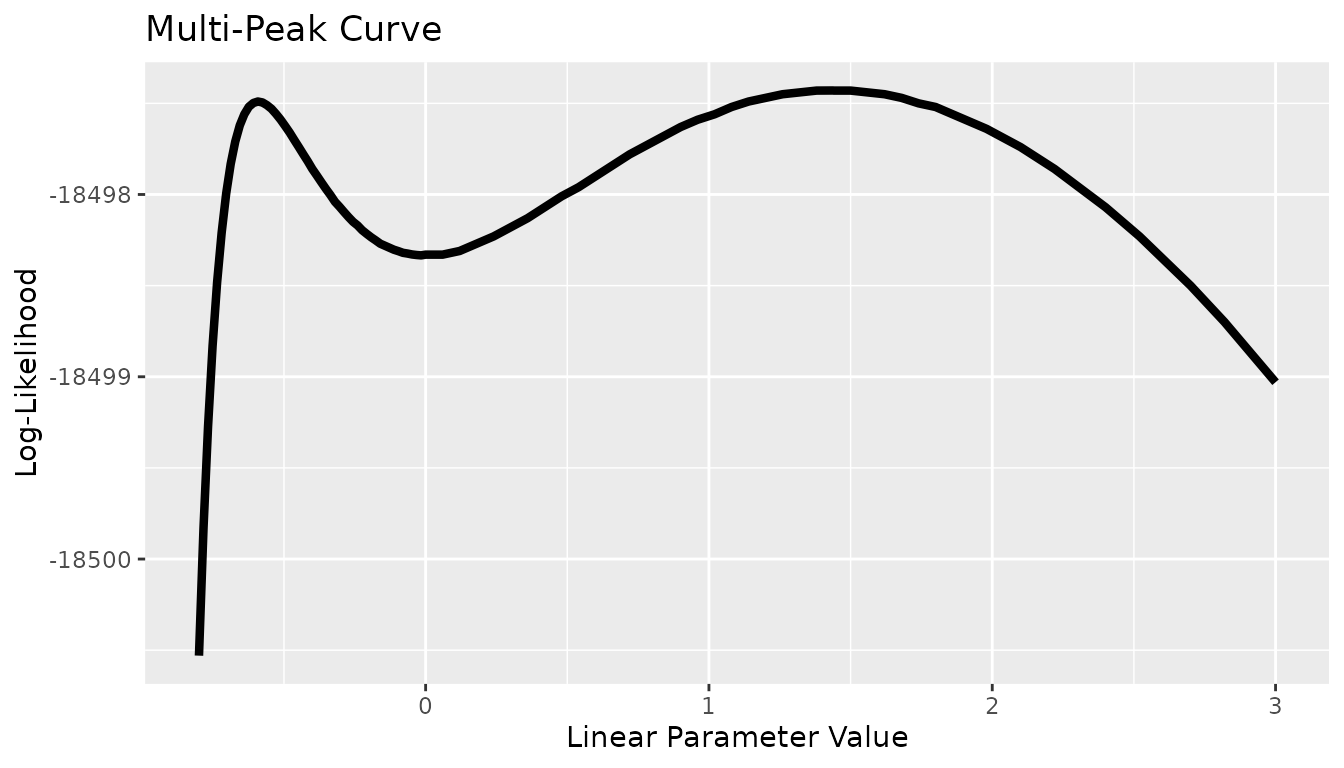

#> |--------------------------------------------------------------------------------|Illustration of Issues with Likelihood-Boundary Algorithm

One important thing to keep in mind is that the likelihood-based

boundary algorithm is not perfect, and at times it may be important to

manually solve for the likelihood curve. The following example outlines

how this is done and what details about the curve can cause issues for

the boundary algorithm. The following uses a dataset used by

Colossus for unit testing. The linear parameter was

selected for analysis. For each point on a grid, the linear parameter

was fixed and the model was optimized.

fname <- "base_example.csv"

df <- fread(fname)

keep_constant <- c(0, 0, 1)

a_n <- c(-1.493177, 5.020007, 1.438377)

model <- Cox(entry, exit, event) ~ loglinear(dose0, dose1, 0) + linear(dose0, 1)

#

control <- list(

ncores = 1, lr = 0.75, maxiters = c(100, 100), halfmax = 5,

epsilon = 1e-6, deriv_epsilon = 1e-6, step_max = 1.0,

thres_step_max = 100.0, verbose = 2,

ties = "breslow"

)

v0 <- sort(c((0:50 / 50 - 1.0) * 0.8, 1:50 / 50 * 3, 1.438377, -0.5909))

for (v in v0) {

a_n <- c(-1.493177, 5.020007, v)

e <- CoxRun(model, df, a_n = a_n, control = control)

ll <- e$LogLik

beta <- e$beta_0

print(c(ll, beta[3]))

}What is important to note is that there are two local optimums within a small range (-0.6 and the global solution at 1.4). The algorithms used for solving the likelihood boundary, similar to the standard regression optimizing algorithm, can be trapped by local optimums. This means that if the algorithm at any point has to cross over the local optimum, it can get stuck. The two optimums have scores close enough that a 95% confidence interval has a lower boundary below -0.5, but a 50% confidence interval has a lower bound between -0.5 and 1.4. This meant that the algorithm converged to the 50% confidence interval boundary, but failed to converge for the lower boundary of the 95% confidence interval boundary. Development is ongoing to automate the process for solving the complete likelihood curve.

x <- c(-0.8, -0.784, -0.768, -0.752, -0.736, -0.72, -0.704, -0.688, -0.672, -0.656, -0.64, -0.624, -0.608, -0.592, -0.5909, -0.576, -0.56, -0.544, -0.528, -0.512, -0.496, -0.48, -0.464, -0.448, -0.432, -0.416, -0.4, -0.384, -0.368, -0.352, -0.336, -0.32, -0.304, -0.288, -0.272, -0.256, -0.24, -0.224, -0.208, -0.192, -0.176, -0.16, -0.144, -0.128, -0.112, -0.096, -0.08, -0.064, -0.048, -0.032, -0.016, 0.0, 0.06, 0.12, 0.18, 0.24, 0.3, 0.36, 0.42, 0.48, 0.54, 0.6, 0.66, 0.72, 0.78, 0.84, 0.9, 0.96, 1.02, 1.08, 1.14, 1.2, 1.26, 1.32, 1.38, 1.438377, 1.44, 1.5, 1.56, 1.62, 1.68, 1.74, 1.8, 1.86, 1.92, 1.98, 2.04, 2.1, 2.16, 2.22, 2.28, 2.34, 2.4, 2.46, 2.52, 2.58, 2.64, 2.7, 2.76, 2.82, 2.88, 2.94, 3.0)

y <- c(-18500.53, -18499.829, -18499.273, -18498.831, -18498.482, -18498.21, -18497.995, -18497.832, -18497.71, -18497.621, -18497.56, -18497.519, -18497.498, -18497.49, -18497.4904, -18497.495, -18497.51, -18497.53, -18497.558, -18497.589, -18497.624, -18497.66, -18497.7, -18497.739, -18497.779, -18497.818, -18497.86, -18497.896, -18497.933, -18497.969, -18498.003, -18498.04, -18498.067, -18498.096, -18498.124, -18498.15, -18498.17, -18498.196, -18498.216, -18498.235, -18498.252, -18498.27, -18498.281, -18498.292, -18498.303, -18498.311, -18498.32, -18498.324, -18498.329, -18498.332, -18498.334, -18498.33, -18498.33, -18498.31, -18498.27, -18498.23, -18498.18, -18498.13, -18498.07, -18498.01, -18497.96, -18497.9, -18497.84, -18497.78, -18497.73, -18497.68, -18497.63, -18497.59, -18497.56, -18497.52, -18497.49, -18497.47, -18497.45, -18497.44, -18497.43, -18497.429487, -18497.43, -18497.43, -18497.44, -18497.45, -18497.47, -18497.5, -18497.52, -18497.56, -18497.6, -18497.64, -18497.69, -18497.74, -18497.8, -18497.86, -18497.93, -18498.0, -18498.07, -18498.15, -18498.23, -18498.32, -18498.41, -18498.5, -18498.6, -18498.7, -18498.81, -18498.92, -18499.03)

df <- data.table(x = x, y = y)

if (system.file(package = "ggplot2") != "") {

g <- ggplot2::ggplot(df, ggplot2::aes(x = .data$x, y = .data$y)) +

ggplot2::geom_line(color = "black", alpha = 1, linewidth = 1.5) +

ggplot2::labs(x = "Linear Parameter Value", y = "Log-Likelihood") +

ggplot2::ggtitle("Multi-Peak Curve")

} else {

g <- message("ggplot2 wasn't detected. Please install to see the plot")

}

g

Likelihood Boundary Algorithm Alternative

There are three functions available for calculating likelihood-based boundaries. The first method is the standard Venzon-Moolgavkar algorithm. This method attempts to both optimize the model and guide the desired parameter to the boundary value. This method is the fastest, but most susceptible to local extrema. Using this algorithm depends on the initial step not being close to a local extrema, so the initial step can be scaled up or down.

The second method is a modification of the Venzon-Moolgavkar algorithm. In the second method, the initial step is split into multiple guesses, and each guess is optimized independently. The Venzon-Moolgavkar algorithm is then continued at the closest guess that did not exceed the target likelihood. In theory, this method makes it more likely for the algorithm to start at an appropriate point, so it is slower but slightly less susceptible to local extrema. However the final portion of the algorithm is still based on derivatives, so it is still susceptible to local extrema.

The third method is an iterative bisection method. In this algorithm, the desired parameter is fixed, and the model is optimized at the endpoints of an interval until an interval is located which contains the goal likelihood. Then the interval is split in half until the interval width is within a user-set limit. This method takes advantage of the fact that the likelihood curve is continuous and we know that the optimum point must be above the goal. The algorithm is split into two steps: optimizing the model at fixed points and determining if the interval contains the goal. The second step does not depend on the likelihood derivatives, so it is not prone to getting stuck in local extrema. However, the interval width must be small enough not to step over the solution. Given a small enough interval width, every optimization is likely to converge and the solution is unlikely to be skipped. This method requires the model to be optimized repeatedly, so it is expected to take the longest. However, the bisection method is the least likely to have issues converging.

fname <- "base_example.csv"

df <- fread(fname)

model <- Cox(entry, exit, event) ~ loglinear(dose0, dose1, 0) + linear(dose0, 1)

keep_constant <- c(0, 0, 0)

a_n <- c(-1.493177, 5.020007, 1.438377)

#

control <- list(

ncores = 1, lr = 0.75, maxiter = 100, halfmax = 5,

verbose = 2

)

coxres <- CoxRun(model, df, a_n = a_n, control = control)

curve_control <- list(maxstep = 20, alpha = 0.005, para_number = 3, step_size = 0.5, bisect = TRUE)

e <- LikelihoodBound(coxres, df, curve_control, control = control)Expected Information Matrix Derivation

The expected information matrix is calculated using two equations, the second derivative of log-likelihood and the probability of a subject having an event given the rows at risk and the number of events. To begin, the second derivative of log-likelihood is expressed as follows:

Next, we assume we have independent failure and censoring, and events in a risk group . Assuming each row at risk has an approximately equal background rate, the probability of any given subject having an event is as follows:

Finally, we want to evaluate the expected information matrix given the following:

We can start by splitting the equation into the expected contribution at each event time () and then simplifying the expected value of constant terms. Note that we switch from the event indicator of each row () to the number of events in each risk group ():

Finally, we substitute, cancel, and use the function definitions above and we have the expected information matrix derived from the observed information matrix formula.